The EU’s new Markets in Crypto Assets (MiCA) framework has laid the groundwork for Europe’s next phase in digital finance, setting clear rules for crypto-assets and redefining compliance rules for cross-border payrolls. In response to such momentum, a consortium of European banking institutions launched a euro-dominated stablecoin in September, 2025, in an effort to counter U.S. dominance in digital payments, although most stablecoins in circulation remain backed by the U.S. dollar.

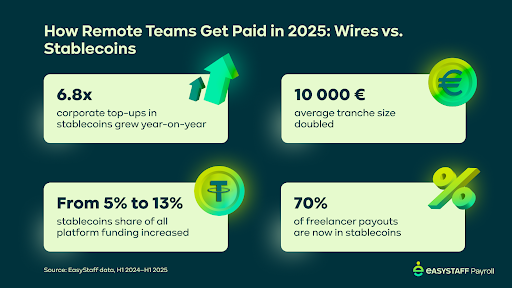

Now, a new report by EasyStaff, a company specialised in streamlining remote payments, reveals such efforts are paying off. According to the study, the global adoption of stablecoins for payroll surged in the first half of 2025, with 70% of freelancer payouts being made in stablecoins. The volume of corporate deposits also rose nearly sevenfold in just one year, climbing from 5% to 13%.

No more traditional payments?

As more teams decide to hire abroad and increased demand emerges for efficient and fast cross-border payments, traditional banking systems have been increasingly rejected. And while the U.S. continues to dominate in the field, Europeans have a chance at digital dominance.

At the operational level, the shift away from traditional rails- conventional financial infrastructures- such as SWIFT or SEPA, brings about important improvements in speed and cost-effectiveness. Vitalii Mikhailov, founder and CEO of EasyStaff, explained that stablecoin transactions in remote payroll “take minutes, not hours or days, and costs are usually lower depending on provider and corridor,” while in conversation with 150sec.

“[Stablecoin transfers] offer faster reconciliation, stronger FX control, and flexible payout rails by jurisdiction and urgency,” he added. In using stablecoins, EasyStaff can pay workers anywhere in the world quickly, avoiding burdensome fees.

{kind=link}

With many remote workers based in countries with weaker banking systems, the cryptocurrency offers a stable and reliable alternative to the SWIFT network. As many stablecoins are pegged to the U.S. dollar or other strong currencies, they may provide a more reliable store of value and a hedge against high inflation, serving even as an alternative to local currencies.

Adoption hurdles

Adopting these new payment practices brings its own set of challenges, however, particularly in terms of compliance, regulation and security. In the traditional banking system, compliance responsibilities are outsourced to banks.

“With stablecoins, companies must bring those same controls in-house, from sanction screening of wallets, to proving audit trails and securing custody,” explained Niklas Rosvall, Chief Product Officer at the financial crime prevention organisation Trapets, while in conversation with 150sec.

“The sender becomes responsible for anti-money laundering (AML) and sanctions checks.”

Indeed, companies adopting stablecoin funding run a greater risk of failing to comply with AML and countering the financing of terrorism (CFT) norms. The likelihood of mis‑screening counterparties increases, and it becomes harder to apply the EU Transfer of Funds Regulation’s crypto Travel Rule, according to which the sender’s and receiver’s information must travel with transactions. With stablecoin payments, no central entity automatically verifies the recipient, making compliance checks harder.

Security concerns are similarly placed on the shoulders of payers and payment intermediaries: safeguarding corporate stablecoin deposits and ensuring secure custody are no longer the sole responsibility of banks. As Rosval points out, “In SWIFT, the bank keeps your money safe. With stablecoins, you’re responsible for securing the private keys — lose them, and you lose the funds.” Companies must now make secure wallet practices a priority.

MiCA, a lever for the future of payment

Fully applicable since December 2024, the MiCA Regulation sets rules for issuing, trading, and providing services with crypto-assets- including stablecoins- to ensure financial stability and market integrity. By placing stablecoins on par with fiat currencies, the regulation harmonises practices across the EU space, enabling compliance leaders to standardise controls rather than being forces to reinventing them country by country. The framework also strengthens security and stability, as issuers must ensure proper reserves, redemption rights, and transparency.

European financial institutions are spearheading efforts to adapt to the stablecoin boom. Most recently, nine banks- including Italian Banca Sella, Belgian KBC, and Spanish CaixaBank- joined forces to launch a MiCAR-compliant euro-denominated stablecoin, seeking to become a trusted payment method in the digital ecosystem. Others have been more cautious, with Francois Villeroy de Galhau, governor at the Banque de France, calling for efforts to maintain the sovereignty of central banks in spite of stablecoins.

Baran Ozkan, Co-founder and CEO of AI-native transaction monitoring company Flagright, puts it simply: “Think of MiCA as a quality bar. If you pay teammates in the EEA, you must check that the token is an EU‑authorised e‑money […] or asset‑referenced, and that your provider is licensed. That buys you clear disclosure, strict reserve rules, and a legal right to redemption at face value.”

A reactive approach

Building on MiCA, the European Central Bank (ECB) has been working to counteract the dominance of USD-pegged stablecoins and the threats it poses to European financial sovereignty. The launch of EUROC and EURS, euro-backed stablecoins, highlights the demand for a currency anchored by the euro to support strategic autonomy in payments.

The ECB fears that privately issued stablecoins could undermine monetary policy and financial stability, and has announced the launch of a digital euro, which commercial banks worry could shrink deposits should customers move funds into central bank digital currency instead of traditional accounts.

In the meantime, the changing landscape of cryptocurrencies challenges companies like EasyStaff to preserve efficiency while adhering to more stringent compliance regulations. As per Mikhailov’s, “the key challenge is to adapt treasury and legal frameworks to fast-changing regulations while staying audit-ready and payout-flexible.”

Global payments are shifting from traditional systems to faster, more flexible alternatives. Multi-rail treasury strategies are becoming the new norm, with wires, cards and stablecoins all used side by side.

And while the widespread adoption of stablecoin in cross-border team payments undoubtedly improves efficiency, the growing use of U.S.-pegged stablecoins also raises major concerns in Europe: competition with domestic currencies, deposit outflows from banks, greater exposure to US Treasuries, and fiscal revenue erosion.

Beyond these immediate concerns, experts warn that such trends could eventually threaten European monetary sovereignty, as technologies driving innovation risk shifting control and seigniorage profits from public institutions to a few private global actors.

Featured image: Masood Aslami via Unsplash